Vulnerable Customer Policy - All Companies - Group Compliance

Title: Vulnerable Customer Policy (All Companies) Author: Group Compliance Department Version: 2 Created: October 2017 Last Reviewed: September 2022

1. INTRODUCTION AND PURPOSE

1.1 The FCA and CBI expect firms to ensure that the fair treatment of vulnerable customers is properly embedded within their culture, policies and procedures. The FCA Principles for Business (PRIN) and the CBIs Consumer Protection Code require firms to treat their customers fairly, however particular care should be taken where the customer is vulnerable as their individual circumstances could limit their ability to make reasonable decisions. The aim of the guidance is to ensure that vulnerable customers receive outcomes as good as those for other customers.

2. SCOPE

2.1 The Groups policy applies to all FCA and CBI regulated firms, involved in the supply of services and products to all customers who have characteristics of vulnerability.

3. OUR COMMITMENT

As a Group we commit to ensuring the fair treatment of vulnerable customers is embedded as part of a healthy culture from senior leadership through to the frontline staff. To do this we will ensure that:

• We understand the needs of our target market / customer base.

• Our staff have the right skills and capability to recognise and respond to the needs of vulnerable customers.

• We respond to customer needs and consider vulnerable customers throughout product design, customer service provision and communications.

• We monitor and assess whether they are meeting and responding to the needs of customers with characteristics of vulnerability, and make improvements where this is not happening.

4. DEFINITION OF A VULNERABLE CUSTOMER

4.1. Our definition of a ‘vulnerable customer’ is:

“Someone who, due to their personal circumstances, is especially susceptible to harm, particularly when we have not acted with appropriate care”. This can include:

a) Customers who have the capacity to make their own decisions but who, because of individual circumstances, may require assistance to do so; and/or

b) Customers who have limited capacity to make their own decisions and who require assistance to do so.

The FCA have identified four key drivers which may increase the risk of vulnerability:

• Health: health conditions or illnesses that affect the ability to carry out day to day tasks;

• Capability: low knowledge of financial matters or low confidence in managing money (financial capability). Low capability in other relevant areas such as literacy or digital skills;

• Resilience: low ability to withstand emotional or financial shocks;

• Impact of a life event: major life events such as bereavement, job loss or relationship breakdown.

Vulnerable customers may fall into two categories:

4.2. In terms of identifying vulnerable groups who may need or want to access our services, the following list gives possible examples of vulnerable customers. It is not intended to be exhaustive but merely illustrative. There are further details in Appendix 1.

4.3. Our aim is to consider each customer’s circumstances and strive to deliver excellent customer service whilst making the necessary adjustments to our processes. We recognise that there can be no set criteria to define vulnerability and no standard response.

5. OUR PRINCIPLES

5.1 In developing procedures and policies for dealing with vulnerable customers we have paid due regard to the principles outlined in the FCA guidance for firms on the fair treatment of vulnerable customers - FG21/1, Occasional Paper 8 – Consumer Vulnerability and Money Advice Trust and Money Advice Liaison Group guide on Vulnerable Customers, Data Protection and Disclosure and Consumer Protection Code 2012.

5.2 To ensure that vulnerable customers are treated fairly and appropriately we will:

a) Understanding Customer Needs

• Understand the nature and scale of vulnerability that exists within our target market/customer base and understand the impact of vulnerability on the needs of customers target market/customer base including the types of harm that may be faced or how vulnerability may affect customer experience and outcomes.

b) Skills and Capability

• Embed the fair treatment of customers across all business areas and ensure all staff understand how their role may affect vulnerable customers.

• Ensure that frontline staff are trained to recognise and respond to a range of characteristics of vulnerability.

• Provide the appropriate practical and emotional support to frontline staff dealing with vulnerable customers

c) Product and Service Design

• Ensure that we consider the needs of vulnerable customers at all stages of our product and service design process, including idea generation, development, testing, launch and review to ensure products meet their needs.

• Consider the potential positive and negative impacts of a product or service on vulnerable customers and look to design them to avoid potential harmful impacts.

d) Customer Service

• Setup our processes and systems to encourage and support customers in disclosing potential vulnerabilities to us.

• Tailor our processes and systems to deliver appropriate customer service that responds flexibly to the needs of vulnerable customers.

• Make customers aware of the support available to them including 3rd party and specialist support services where available

• Put in place systems and processes that support delivery of good customer service including tools to note and retrieve information on a customer’s needs

e) Communications

• Ensure all communications and information about products and services are understandable to customers in our target market/customer base.

• Consider how we communicate with vulnerable customers, taking into consideration their needs. Where possible offering multiple channels so customers have a choice.

f) Monitoring and Evaluation

• Implement appropriate processes to evaluate where we are not meeting the needs of vulnerable customers so we can undertake improvements

• Produce and regularly review MI on the outcomes that we deliver for vulnerable customers.

6 COMPANY EXPECTATIONS

6.1 We recognise that all our customer-facing staff need to be alert to the signs that the person they are talking to may not have the capacity, at that moment in time, to make an informed decision about the implications of the decisions that they are being asked to make. We expect that this should be an extension of the existing skills of listening and identifying needs and adjusting their approach accordingly.

6.2 We expect all staff to:

• Meet the expectations of the relevant Principles of Business and Code of Conduct applicable to their business area.

• Treat customers fairly and with dignity and respect at all times. • Assess the needs of customers on an individual basis and tailor the service provided to meet those needs.

• Actively listen out for information that could indicate vulnerability and, where relevant, seek additional information.

• Take ownership and focus on gaining the best possible outcome for the customer.

• Seek additional support from their line manager or appropriate business area where required to assist the customer.

• Ensure customer records are updated to note when a customer is to be treated as vulnerable and any specialist measures applied as a result.

6.3 Managers, Supervisors and Teams Leads have responsibility to:

• Support their staff in meeting the expectations above.

• Ensure that staff complete any training related to vulnerable customers when set by Group Training.

• Where a vulnerability is suspected and the customer may have or presents signs of financial difficulties, where the premium has been arranged via premium finance, inform the premium finance company of the potential vulnerability.

• Decide what additional measures may be needed to support a vulnerable customer beyond the standard processes in place and to seek additional support from other Group Functions where appropriate.

6.4 Senior Managers and Department Heads have responsibility to:

• Consider whether the products or services being offered by their business area are suitable for the needs of vulnerable customers.

• Ensure that staff complete any training related to vulnerable customers when set by Group Training.

• Consider vulnerable customers when developing or amending policies and processes.

• Encourage a culture of treating customers fairly and supporting the needs of vulnerable customers in their business area.

6.4 Group Compliance and Audit functions have responsibility to:

• Annually review and update the Groups Vulnerable Customer Policy.

• Provide advice and support to other business areas in dealing with vulnerable customers.

• Carry out appropriate audit checks on the fair treatment of vulnerable customers and provide feedback on any issues identified.

• Monitor complaint/conduct risk MI and flag any matters of concern or identified trends to the relevant Senior Manager and/or Department Head, audit committee and board meetings.

• Consider the fair treatment of vulnerable customers during reviews of Group policies and when signing off financial promotions and customer communications.

6.5 Group Training have responsibility to:

• Implement appropriate training at induction and on an on-going basis on the fair treatment of vulnerable customers.

7 APPROACH TO VULNERABILITY

7.1 Whenever we interact with customers, we must treat them with respect, as individuals, and recognise that any customer may be vulnerable. Our aim is to provide to all our customers well-designed, straightforward, understandable products and services that respond to individual circumstances.

7.2 Applying a sympathetic approach which is both sensitive to and reflects the needs of vulnerable customers is necessary to ensure that:

• Information provided to customers is clear and transparent;

• The service provided to customers is consistent with the service they should reasonably expect;

• When things go wrong they are put right and action is taken to stop the same thing being repeated;

• Customers are not taken advantage of.

7.3 Further practical guidance can be found in Appendix 1.

8 RECORD KEEPING

8.1 Where we establish that a customer is vulnerable and requires assistance, this should be recorded on the system in accordance with team/system process to avoid the customer having to repeat disclosure and explanation at each interaction with us and enable us to be more responsive to the customer’s needs.

8.2 Reasonable concerns about an individual’s ability to manage their own affairs can be noted and must be noted in a professional manner and staff should avoid noting opinions or adding additional subjective comments.

8.3 Where appropriate and possible, a flag is to be placed on the system to identify this clearly at the outset to assist future interactions with the customer. Explicit consent needs to be obtained from a customer prior to recording any sensitive personal data.

9 FURTHER QUERIES

9.1 If you have any queries on this policy then please raise them with your Line Manager in the first instance.

9.2 Appendix 1 outlines guidance in relation to what staff should look out for, tips for talking to potentially vulnerable customers and considerations to make pre-sale or when dealing with ongoing administration.

10 RELATED DOCUMENTS

• Principles for Business Policy • Code of Conduct Policy (SMCR) UK

APPENDIX 1 - GUIDANCE FOR FRONTLINE STAFF IN DEALING WITH VULNERABLE CUSTOMERS

1. RECOGNISING VULNERABLE CUSTOMERS

1.1. All customers are at risk of becoming vulnerable, but this risk is increased by having characteristics of vulnerability. When we refer to vulnerability, we typically mean that a person has one or more of the characteristics that places them at higher risk of harm if something goes wrong or if we don’t act with appropriate due care and attention

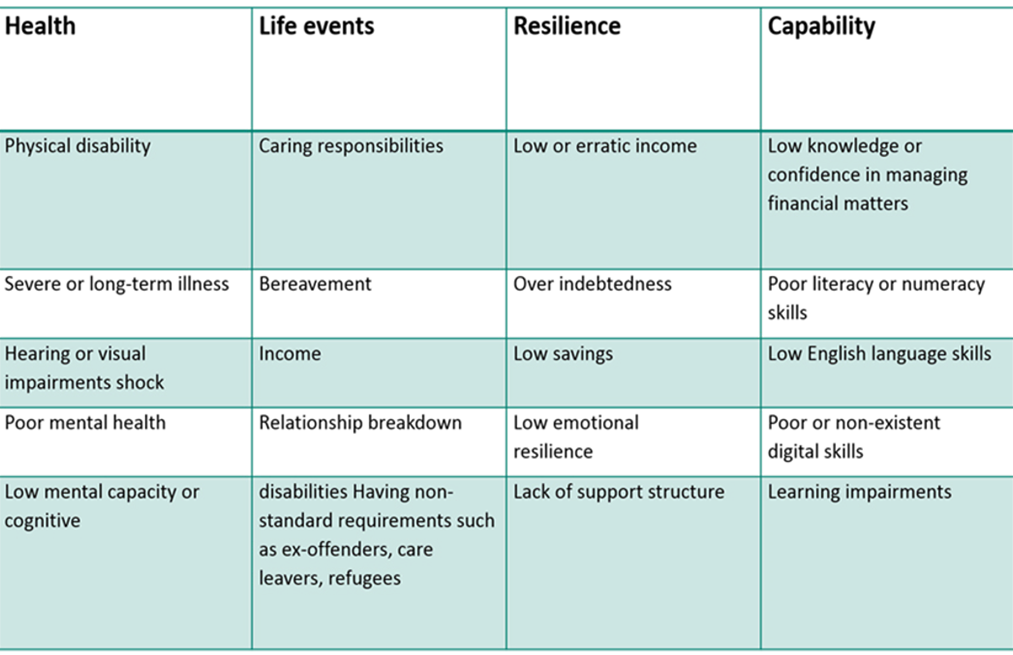

1.2. We breakdown these characteristics into four key areas ; Health, Life Events, Capability and Resilience. There are some examples of each shown below. This is neither a prescriptive nor exhaustive list, but rather a sample of indicators that might suggest that a customer is vulnerable:

a) Health: impaired ability to make a decision or to deal with us effectively due to mental or physical health conditions with examples being:

• A mental health condition (e.g., dementia, anxiety, depression)

• A physical disability or old age where the individual requires support to manage their day-to-day decision making or activities (e.g., blindness, deafness)

• Long-term or chronic illnesses

• Injury after an accident. This can include short term injuries that will heal but still impact a person’s ability to carry out activities like they used to

b) Life Events: major life events that impact on a person’s ability to make decisions or manage their affairs such as:

• Bereavement

• Relationship breakdown and divorce

• Taking on caring responsibilities

• Redundancy and loss of employment

• Criminal prosecution, being sent to prison

• Bankruptcy

c) Capability: this can involve a person lacking some of the skills, knowledge or understanding to allow them to engage with us effectively. This can include:

• Poor reading or mathematics skills

• English not being the customer’s first language

• Learning difficulties

• Poor digital skills and/or limited access to digital tools such as a home computer, smart phone, internet access, email account etc.

d) Resilience: Customers who may lack the ability to withstand emotional and/or financial shocks, such as:

• Low or erratic income including people on zero hours jobs or working in the “gig” economy

• High levels of debt

• No or low levels of savings

• Lack of a support network to assist in difficult situations

• Low emotional resilience and ability to cope with stressful situations

1.3. Not everyone who has one of these characteristics will automatically be vulnerable, but it is important we look out for these factors.

For many vulnerable customers the situation will be complex and involve overlapping characteristics. For example,

Mr Smith gets into a serious car accident (life event), it leaves him injured so unable to work (health, resilience). Mr Smith worked as a self-employed fitness instructor so is only paid when he works, has no savings and no sick pay (resilience). The stress of the matters leads to him becoming depressed and anxious (health) and he finds it hard to deal with people over the phone (capability).

1.4. It can be difficult to identify that a customer is vulnerable when speaking to them on the phone, when transacting online or when dealing with written communications where non-verbal signals (facial expressions and body language) are not visible.

It is important always to listen carefully to customers on the phone and ensure we make them feel that we are approachable if they want to discuss matters.

Should we have concerns regarding the type of communication channel used then we should ensure the customer is aware of the other channels open to them. It might be appropriate to arrange a phone call, or direct them to written or online communications depending on the customer needs / requirements..

For those customers choosing the on-line option due to hearing difficulties, the option of us speaking with a third party or communicating in writing or through email should be considered.

2. WHAT SHOULD CUSTOMER FACING STAFF BE LOOKING FOR IN ORDER TO IDENTIFY WHETHER A CUSTOMER IS VULNERABLE?

• They ask you to speak up or speak more slowly

- Can they hear the complete conversation or are they missing important bits? - Do they understand what you are saying?

• They appear unusually hesitant or confused

- Do they know what is being discussed? - Do they ask unrelated questions? - Do they keep wandering off the point in the discussion and talking about irrelevancies or things that don’t make sense? - Do they keep repeating themselves? - They take a long time to answer questions - Do they say ‘Yes’ in answer to a question when it is clear they haven’t listened or understood?

• They take a long time to get to the phone and sound flustered or out of breath, indicating they may have a lack of mobility due to age or illness

• They say “My son/daughter/wife/husband etc deals with these things for me”

• Where there is a language barrier, or they need someone to translate for them

• They say that they don’t understand their bill, a previous phone conversation or recent correspondence

• Has the customer’s payment behaviour changed with payments being missed or are they using phrases like:

- I can’t pay or I’m having trouble paying - Can I take a break in my payments - Can I bring down my payments or reduce costs mid-term

• The customer seems distracted, rushed or pre-occupied when you are trying to talk to them

• They make reference to a life event or are making policy changes that indicate one may have happened i.e.:

- Taking a driver off the policy - Notifying of a death - Changing their relationship status - Changing occupation especially from paid employment to unemployed - Reporting a claim - Advising of a medical condition, criminal conviction, or bankruptcy especially if it was not disclosed before

3. SOME TIPS FOR TALKING TO POTENTIALLY VULNERABLE CUSTOMERS

• Speak in a plain and simple manner and try to pronounce what you say in as clearly as possible

• Avoid using jargon, abbreviations, or industry terminology that the customer may not understand

• Set expectations for the conversation or call – outline all the information that will be required – account numbers, personal details, etc – and how long the call is likely to last. As the “experts” we should guide the call to keep it ‘on topic’

• Be patient and empathise with the customer. Let them know we are approachable and what to help

• Don’t rush them, if they need to put the phone down to find account details it could take them some time. Give the customer time to explain fully, don’t interrupt or show impatience

• Don’t assume that you know what the customer needs – it’s easy to rush through if the customer is slow or not able to explain what they need

• Clarify understanding at every point posing the question “is there anything you’d like me to explain?”. Ask the customer r to explain to you what they understand the agreement to be.

• If we need more information or are unsure about anything the customer has told us make sure to ask them. Avoid guessing or trying to interpret unclear answers or information as this can result in misunderstandings

• Don’t assume that the person you are talking to is sighted, can hear everything you are saying or can easily call to a branch – the customer could have health issues that are not obvious on the phone so always ask if what we are doing is ok and offer alternatives where possible. i.e. “I’ll send your documents by email, is that ok?” or “ We need a copy of your diving licence, you can post it in, email us a copy or call into branch, which suits you best?”

• Listen for what isn’t being said, not just what is – e.g., absence of price, commitment, timing type questions on the part of the person receiving the call should ring alarm bells. Remember that vulnerable customers s can sometimes be forgetful or overly trusting, ask yourself honestly whether a ‘yes’ is real agreement or just submission

• Ask if there is a better time to call – e.g., some people will be in a better position to take a call in the afternoon rather than the morning

• Check the customer’s file for existing notes and information that might help. This can avoid the customer having to repeat themselves or cover difficult topics that they may have already talked about

• Try to take ownership of the case and minimise the need for transferring the call. Rather than transferring a customer it might help for you to ring and speak to the other area on their behalf. When you do transfer make sure you let the next staff member know the details to avoid the customer having to go over things again

• At the end of a call make sure the notes on the file are updated so whoever speaks with the customer next is aware of any vulnerability. Ensure that notes are always written in a professional and objective manner, avoid opinions and assumptions. If you’re not sure what to note down always check with your line manager

4. THINGS TO CONSIDER DURING A SALE OR CLAIMS CALL

• Consider whether the customer demonstrates that they have a general understanding of what decision they need to make and why they need to make it. Do they understand the consequences of making, or not making, this decision? Can they understand and process information about the decision? And can they use it to help them make a decision?

• Ask the following questions: “do you need to discuss this with anyone else?” / “would you like me to explain any part of this call again?” / “do you want to think about this before making a decision?” / “is there anything we can do to assist you with this process?”

• If they say something that suggests they don’t fully understand what you have said, be prepared to repeat or paraphrase to clarify understanding

• Don’t assume that they fully understand all the implications of the offer/agreement. Explicitly and clearly confirm all the important information

• Make sure that the customer is not flustered, agitated or in an emotional state when they make a decision. If they are, suggest that they talk it through with someone else and offer to ring them back. Where appropriate, suggest that a guardian or carer could be present on the call or offer to discuss matters with a trusted third-party carer or family member, if this would help

5. ADDITIONAL SUPPORT

Where you have concerns about a customer that you can’t easily manage using the tools outlined above, then what should you do?

• Refer to your line manager for advice.

• Contact the appropriate business support team that deal with the issue that you have concerns about, i.e. missed payments, speak with Accounts.

• Check if we can send details in an alternative format for them to consider including by email or other electronic format that may allow the customer to use accessibility functions available on many computers, tablets and smart phones or in Braille, Large Print or Audio? (Always check before making any promises to the customer as the options available may vary depending on the document in question).

• If the customer is unhappy or reports having suffered difficulties due to their vulnerability, and wishes to escalate the matter, follow the complaints process

• Where third parties are involved engage with them and seek their support and advice if /available. i.e., refer to the Insurer, loss adjustors, Close Brothers etc

• Refer to the support tools on the Group Intranet for external support from Charities and Government bodies. While we want to help as much as possible, we need to know our limits and should consider if it might help the vulnerable customer to direct them to more specialised, expert services as well

• Just as important as supporting our customers is making sure you look after yourself and your colleagues

If you feel upset or feel that the Vulnerable customer’s circumstances have affected you personally, please raise with it with your Manager and schedule time with them for a de-brief. Always seek additional support if required. Group HR can offer advice and assistance, including Mental Health First Aid support, and details of our Employee Assistance Programme. You can also refer to the support tools on the Group Intranet for specialist services that might be of assistance.