Discount Claw Back

When discount has been applied at New Business, Transferred New Business or Renewal, there may be a time where it is appropriate for a broker to take some of this discount back (Claw Back).

When is appropriate to claw back discounts?

- When discount has been given at inception of a policy and a customer either makes a change resulting in an insurer refund or when a policy is cancelled. The amount of discount to be clawed back should be proportional to the insurer refund. E.g. £100 discount given at the beginning of the policy and policy cancelled after 6 months, the discount clawed back would be approx.. £50

Why do we claw back discount?

- Example scenario: Customer buys a policy with an inexperienced additional driver for £2,700 (£3,000 – 10% NB Discount). Later the same day the customer decides to remove the inexperienced driver, the insurer refund is calculated from the premium before discount. In this scenario the insurer premium for insured only driving is £300. As the insurer refund is calculated from the £3,000 and the premium the refund would be £2,700. If a broker didn’t claw back any discount the customer would have paid £2,700 and received a refund for £2,700 therefore effectively paying nothing for a years insurance.

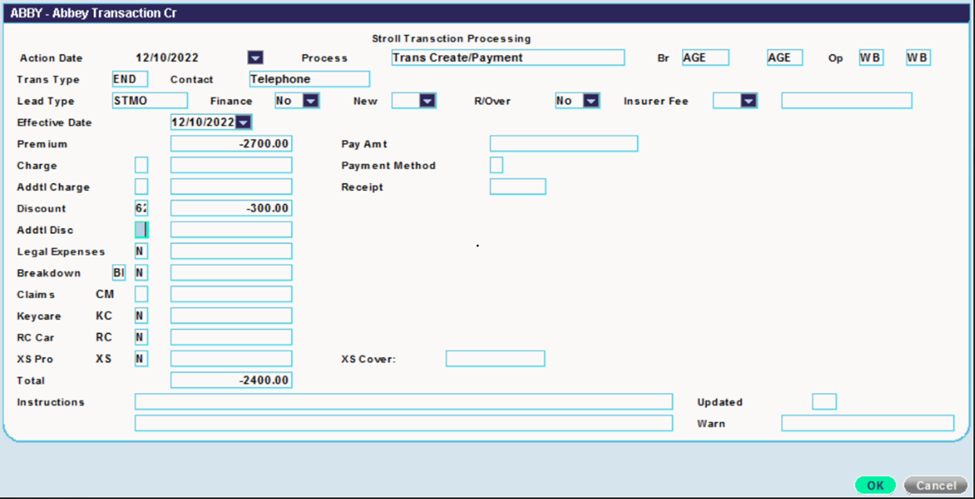

How do I claw back discount in the ABBY frame?

- Guidance from the groups Systems department is that you should enter the discount to be clawed back as a negative amount and use the same discount code that was used when the discount was applied at inception